homer_simpson

Well-known member

blacklist for what?

ps9 said:Looks like I'm refi'ing too much, my broker just said we have to wait a few days to stay off Chase's blacklist, even though we're greenlight to close today.

The California Court Company said:ps9,

so your new lender is NOT Chase, but plan to sell your loan to Chase, and you had a loan with Chase in the last 180 days, you cannot proceed with your refi?

How does waiting an extra couple days make any difference?

ps9 said:The California Court Company said:ps9,

so your new lender is NOT Chase, but plan to sell your loan to Chase, and you had a loan with Chase in the last 180 days, you cannot proceed with your refi?

How does waiting an extra couple days make any difference?

The bank is Chase, current loan and also future loan. Residential Wholesale immediately moves it to CHASE after COE. I believe what my broker is trying to say is Chase will blacklist people who refi too frequently. I'm on the books with Chase because my last refi was less than a year, so in a few days I will come off the 180 days list and when I close escrow Chase will not flag me as a repeat refiler.

Soylent Green Is People said:ps9 - Taxes are payable when you're within 30 days of your 1st payment. Given when you're thinking of closing, your first payment will likely 4/1/15.

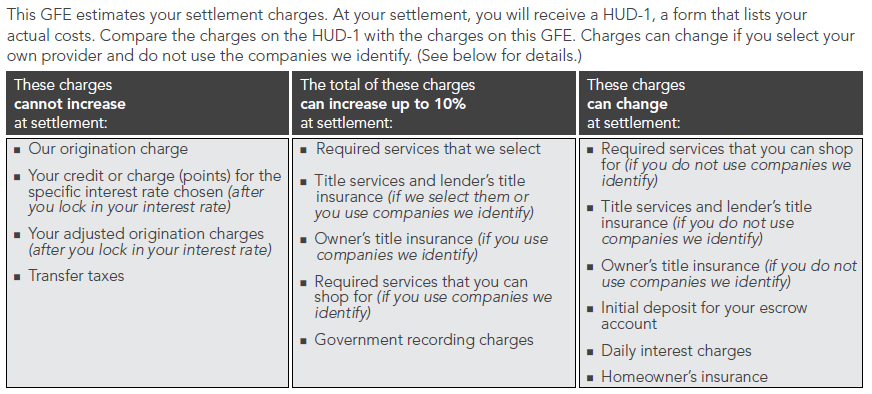

As for Title and Escrow, those fees are X in the Good Faith Estimate. If they are X+ at closing, the lender or escrow (whomoever misquoted at the initial GFE) has to eat that cost. Review your initial GFE as either those final costs were correctly disclosed up front, or someone's got some 'splanin to do at the lender or escrow.

My .02c

Awesome. Time to splurge that money on your better half for Valentine's Day (or on food ;D)ps9 said:Escrow emailed back, looks like they made a mistake? Stated my lender is on the preferred list, so now the ALTA policy is $660 instead of $1100

ps9 said:Here's the confirmation from Morgan Stanley:ps9 said:USCTrojanCPA said:Can you forward me the MS contact info name?ps9 said:So Morgan Stanley emailed back, it is for jumbo loans only, margin is 1.875% (1.75 for <60%LTV, FICO>740), a no cost refi with enough credits to cover closing costs will increase rates to 2.25%. No impounds.

Alyson also has an IO product, details to come.

I was rereading the Morgan Stanley email sent to me, looks like I got it confused:

Margin is 1.875%, 1-Month LIBOR is currently around 0.168 (lucky!), so the rate would be 2.00% (rounded up or down to the nearest 1/8th). To cover closing costs, I was quoted 2.25% with me getting 1pt offset at closing. Don't need that much to cover costs, so then he suggested a half point at closing, which brings the rate to 2.00%. If you have FICO > 740 and LTV < 60% the rate then becomes 1.90%

Does that make sense? I'm assuming the margin of 1.875% is for no cost refi's. 1.625% is for loans with closing costs. I'll have to check with Morgan Stanley on this. Still no impounds, no prepayment penalties, PHH will service the loan but Morgan Stanley holds it in its portfolio.

If this all holds up, I don't see why I woudn't do it. If LIBOR rates stay low, I'll probably never have to refi again (gasp!) and be able to pay off a significant amount of principal in 10 years.

I PM'd you the contact. I gotta do some more research on this, plus can't really do much since I'm already in a refi. Hopefully this product is still around in 3 months

Alyson emailed back, her IO product is nowhere as good as this, believe the rate is 3.5% no cost for 5/1 IO LIBOR (margin 2.5%).

Mr. ps9,

Please see my answers below. I also wanted to make sure that I mentioned a qualification requirement for our interest only products. We would need to verify in the processing of the loan that you have $500,000 in marketable securities and cash. These funds can be in a checking account, a savings account, an investment account, or retirement accounts. Please let me know if you have any questions. When is your other loan expected to close? Thank you.

1) Confirmed. The rate with a $3,300 credit offset would be 1.90%(1.875%+1 month LIBOR(rounded up or down to the nearest 1/8th ) and then .10% is deducted for LTV<60% and FICO of 740+)

2) If you pay the closing costs, the rate would come down to 1.65%(1.625%+1 month LIBOR(rounded up or down to the nearest 1/8th ) and then .10% is deducted for LTV<60% and FICO of 740+)

3) We could immediately start the process once your other refinance closes

This looks pretty good, the half million in accounts is weird, must be a MS thing, no other lender has mentioned this before, maybe 6 months PITI but not half million. It's like we'll give you this kick ass rate only if you have an escape route.

ps9 said:rkp said:ps9 said:I would be tossing and turning at night if I ever go back to a 30 yr. Refi from a 30 to a 30 is even worse.

Why worse? We are refi'ing 2 years into a new 30 year and will continue paying the same amount we were paying and instead of paying it off in 28 years from now, we will pay it off in 26 years...2 years saved for a few hours of work. Why is that a bad thing?

Because you restart the clock on a 30 yr, most painful in the first 5 years as 2/3 of your monthly goes to interest. What is your interest rate before and after the refi? And if you refi 2 years into your 30 year, why didn't you consider a 5/1????

Soylent Green Is People said:I encourage my customers to refi their new 30 fixed as a 29 or 23 year (AKA "same payoff") term loans. Refinancing a 28 year loan into a new 30 may be the right decision for some, but it will always cost more in the long run unless you decide to prepay agressively. Example of a "same payoff" refi:

")

")