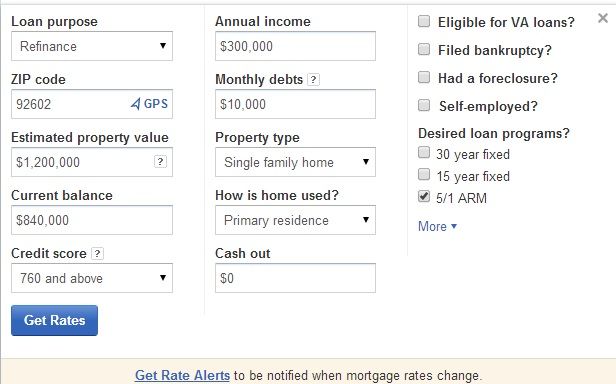

Here's what I got for you at 70%LTV (assuming the inputs below are similar to your own):

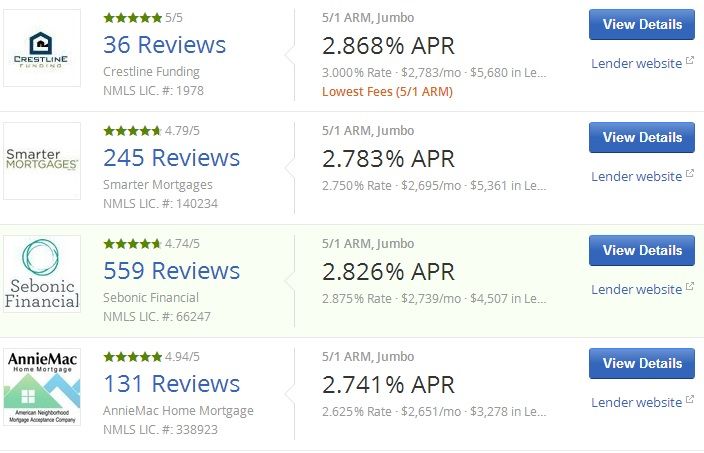

So both lenders can close at 2.875% with more than enough credit to cover all fees, and leftover for your escrow account. You usually need about ~$2500 in lender credit to cover all fees at closing, so you'll come out ahead if you go this route. Annie Mac offers ~$6100 in credit and Sebonic at ~$5100.

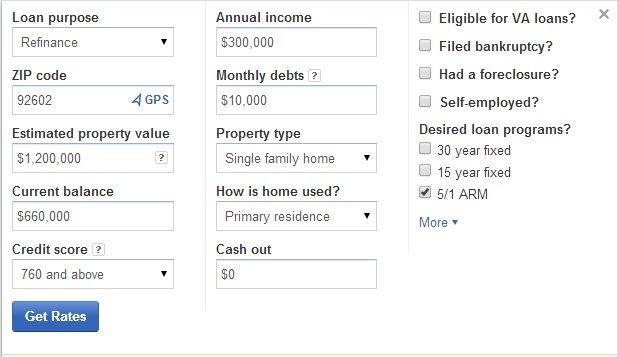

But let's compare at 55%LTV (holding all other variables the same):

Smarter and Annie Mac are the best deals. I would go with the lower rate with less credit. At ~$3200, that's still more than enough to close.

I would check again when markets open tomorrow. Did you submit request thru Zillow? Or did you call Residential Mortgage direct? My deal at 2.5% 5/1 ARM 55%LTV is thru a Zillow request. I saw them post a 2.625% with about $4000 in credit. I put in a inquiry thru Zillow to see if they can do 2.5% with enough credit to cover all fees at closing. They responded, haggled thru email a little back and forth, and finally agreed upon $71 in out of pocket fees for me at closing for the 2.5% rate.

That's why I thought it would be a good deal today, since they posted the same 2.625% rate with the same credit that caught my attention a few weeks ago, I'm thinking the 2.5% would be attainable again.

Good luck, I'll buy you a McRib if you dump your interest bleeding 30 year and refi into a 5/1

")