panda

Well-known member

Trojan,

If Redfin shows that there are currently 838 active listing in Irvine and you are telling me 643, somewhere the numbers are off quite a bit. June of last year the Irvine inventory was at 699, so if your number is correct of 643, we are still within the boundary trend.

You mentioned that 1 - 3 things must occur to see a 10-15% correction in the Irvine Prices. What is your macro economics outlook for the next 20 - 24 months? How probable do you think it is for either 1) moderate/severe US/global recession 2) huge spike in interest rates (above 5%) and/or 3) China imploding to take place by December 31st, 2018?

If Redfin shows that there are currently 838 active listing in Irvine and you are telling me 643, somewhere the numbers are off quite a bit. June of last year the Irvine inventory was at 699, so if your number is correct of 643, we are still within the boundary trend.

You mentioned that 1 - 3 things must occur to see a 10-15% correction in the Irvine Prices. What is your macro economics outlook for the next 20 - 24 months? How probable do you think it is for either 1) moderate/severe US/global recession 2) huge spike in interest rates (above 5%) and/or 3) China imploding to take place by December 31st, 2018?

USCTrojanCPA said:Panda said:Thanks for that info Trojan. Is the Redfin inventory data incorrect then for 838 active listings? If there are 643 homes today, the inventory is slowing growing since December of last year.

Date Inventory

Dec - 2015 484

Jan - 2016 402

Feb - 2016 432

Mar - 2016 505

April - 2016 542

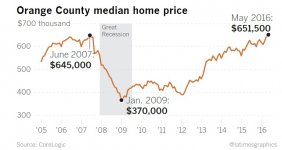

So if you are telling me that inventory levels are at 683 today, inventory in Irvine has risen 70% since January 2016. Let's wait and see what happens to inventory by end of this year. My crystal ball is telling me that there will be 10-15% correction in the Irvine housing market by Dec 31st, 2018.

Not sure where Redfin is pulling their inventory numbers from....I know they have a link to MLS since their site will update within about an hour after I've made chances to my listings on MLS. Anyhow, we are getting lower highs and lower lows on the inventory levels if you looked at it for the past 3-4 years. The low point will be right around new years day and the peak will be around July/Aug. For there to be a 10-15% correction in Irvine prices one or more of a few things have to happen....1) moderate/severe US/global recession 2) huge spike in interest rates (above 5%) and/or 3) China imploding

")