You are using an out of date browser. It may not display this or other websites correctly.

You should upgrade or use an alternative browser.

You should upgrade or use an alternative browser.

How low can we go? 30 yr fixed at 3.75% with no fees...

- Thread starter ps99472

- Start date

NEW -> Contingent Buyer Assistance Program

sgip

Well-known member

Probably not, what with a big fall off in stocks helping rates improve a bit. Point paying might make sense if you're either looking for a higher tax writeoff, combined with a "fix it and forget it" rate for however long you wish keep the home.

PS9,

What are the qualifying guidelines for the Morgan Stanley deal? The rest of their rates are pretty high, beatable even by most mortgage bankers, but the other program is strong, if only for someone with nerves of steel.

My .02c

SGIP

PS9,

What are the qualifying guidelines for the Morgan Stanley deal? The rest of their rates are pretty high, beatable even by most mortgage bankers, but the other program is strong, if only for someone with nerves of steel.

My .02c

SGIP

ps99472

New member

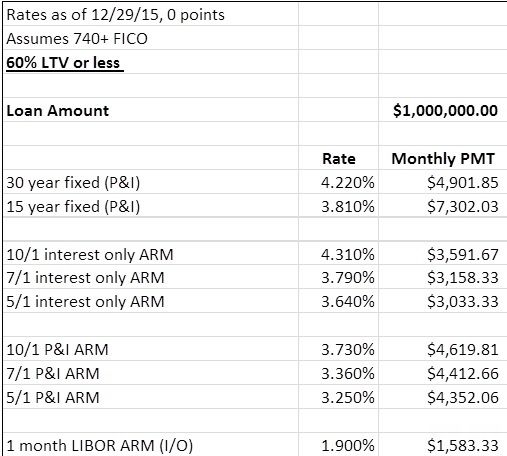

Here's the old flyer from MS

The rate is now 1.90% instead of the 1.75% in the ad. I believe the 0.25 bump is from the fed, and then they discount 0.10 for FICO 740+ and LTV < 60. If you were to do this at no cost, its another 0.25 to get the lender credit which would bring the rate to 2.15%. Looking over my old emails, looks like you can also do a cash out, I would assume without going over the LTV 60.

If I do this... monthly mortgage IO would be around a grand. Make a big principal payment end of year/bonus time.. This might work out.

The rate is now 1.90% instead of the 1.75% in the ad. I believe the 0.25 bump is from the fed, and then they discount 0.10 for FICO 740+ and LTV < 60. If you were to do this at no cost, its another 0.25 to get the lender credit which would bring the rate to 2.15%. Looking over my old emails, looks like you can also do a cash out, I would assume without going over the LTV 60.

If I do this... monthly mortgage IO would be around a grand. Make a big principal payment end of year/bonus time.. This might work out.

Attachments

Perspective

Well-known member

The 10Y UST fell below 2% this morning. Will the 30Y fixed jumbo drop below 3.50%? This is a nice little belated Christmas gift to buyers waiting to lock.

irvinehomeowner

Well-known member

Who are you using?ps9 said:Looks like I'll be refi'ing again, 2.5% 5/1 ARM, thank you China, oil, fed statement, and jittery people.

woodburyowner

Well-known member

Wonder if it's time to play the lender credit game. Basically refi at a higher rate with the largest credit (still needs to be below your current rate) and then immediately refi again at a lower rate, but no cost. This game only works if you believe the rates are going in a downward trajectory.

@ps9, how are you seeing the RWMI rate at 2.5% on zillow? The rates I'm seeing are in the 3s.

@ps9, how are you seeing the RWMI rate at 2.5% on zillow? The rates I'm seeing are in the 3s.

ps99472

New member

RWMI only pops up on Zillow around late morning to afternoon. I saw the 2.625 rate around 10am, emailed Alyson that I'm interested in refi at 2.5 with no cost, she responded that Tues might be lower and she'll update me later at 2pm. Around 4pm I get her email that she got the 2.5% for me and she needs pay stubs, tax return, etc.

My experience is that you gotta move fast (half days time) when 5/1 ARMs get low. Pretty much have a standing application with your broker and give the green light to lock when rates dip.

My experience is that you gotta move fast (half days time) when 5/1 ARMs get low. Pretty much have a standing application with your broker and give the green light to lock when rates dip.

The Motor Court Company

Well-known member

I am still waiting for 30 year fixed to beat my current rate @ 3.25%. will jump back in if it reaches 3%.

by the way my FICO score jumps 10 point into the 800's this month; probably because of the one year anniversary of my last refi - just in time for the upcoming dip this April

by the way my FICO score jumps 10 point into the 800's this month; probably because of the one year anniversary of my last refi - just in time for the upcoming dip this April

sgip

Well-known member

2.625 is about the average for 70% LTV, 780 FICO, $418k and above 5/1 ARM paper. 30 fixed is reaching to 3.625-3.500 fee free under the same conditions. If you bring money, or have assets already with some banks, there's often up to a quarter point reduction available.

The specifics of each deal determine the rate. Example: Some places quote X for SFR's, X+X for Condos or X+x for Detached Condos. As with any source of data on-line the model is often one size fits most, and rarely an exact match. Call to be sure what's on screen is what's on the table.

My .02c

SGIP

The specifics of each deal determine the rate. Example: Some places quote X for SFR's, X+X for Condos or X+x for Detached Condos. As with any source of data on-line the model is often one size fits most, and rarely an exact match. Call to be sure what's on screen is what's on the table.

My .02c

SGIP

Perspective

Well-known member

10Y UST has a one-handle on it again - trading at 1.95% right now. A highly qualified jumbo borrower might be able to lock a 3.25% 30Y fixed purchase loan with minimal fees today.