USCTrojanCPA said:

ps9 said:

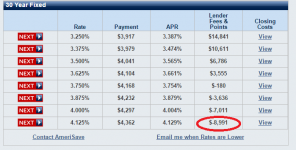

So Morgan Stanley emailed back, it is for jumbo loans only, margin is 1.875% (1.75 for <60%LTV, FICO>740), a no cost refi with enough credits to cover closing costs will increase rates to 2.25%. No impounds.

Alyson also has an IO product, details to come.

Can you forward me the MS contact info name?

I was rereading the Morgan Stanley email sent to me, looks like I got it confused:

Margin is 1.875%, 1-Month LIBOR is currently around 0.168 (lucky!), so the rate would be 2.00% (rounded up or down to the nearest 1/8th). To cover closing costs, I was quoted 2.25% with me getting 1pt offset at closing. Don't need that much to cover costs, so then he suggested a half point at closing, which brings the rate to 2.00%. If you have FICO > 740 and LTV < 60% the rate then becomes 1.90%

Does that make sense? I'm assuming the margin of 1.875% is for no cost refi's. 1.625% is for loans with closing costs. I'll have to check with Morgan Stanley on this. Still no impounds, no prepayment penalties, PHH will service the loan but Morgan Stanley holds it in its portfolio.

If this all holds up, I don't see why I woudn't do it. If LIBOR rates stay low, I'll probably never have to refi again (gasp!) and be able to pay off a significant amount of principal in 10 years.

I PM'd you the contact. I gotta do some more research on this, plus can't really do much since I'm already in a refi. Hopefully this product is still around in 3 months

")

Alyson emailed back, her IO product is nowhere as good as this, believe the rate is 3.5% no cost for 5/1 IO LIBOR (margin 2.5%).